Niger’s Banking Crisis: A Regional Outlier in UEMOA’s Financial Turmoil

The January 2026 economic outlook report for the West African Economic and Monetary Union (UEMOA) delivers a stark warning: while regional banks achieve symbolic milestones, rising risks threaten to undermine stability. Among the eight member states, Niger stands out as a critical weak link, its soaring non-performing loan (NPL) ratio serving as a stark indicator of deepening financial fractures across the bloc.

Niger: The Hardest-Hit Economy in a Fragile Union

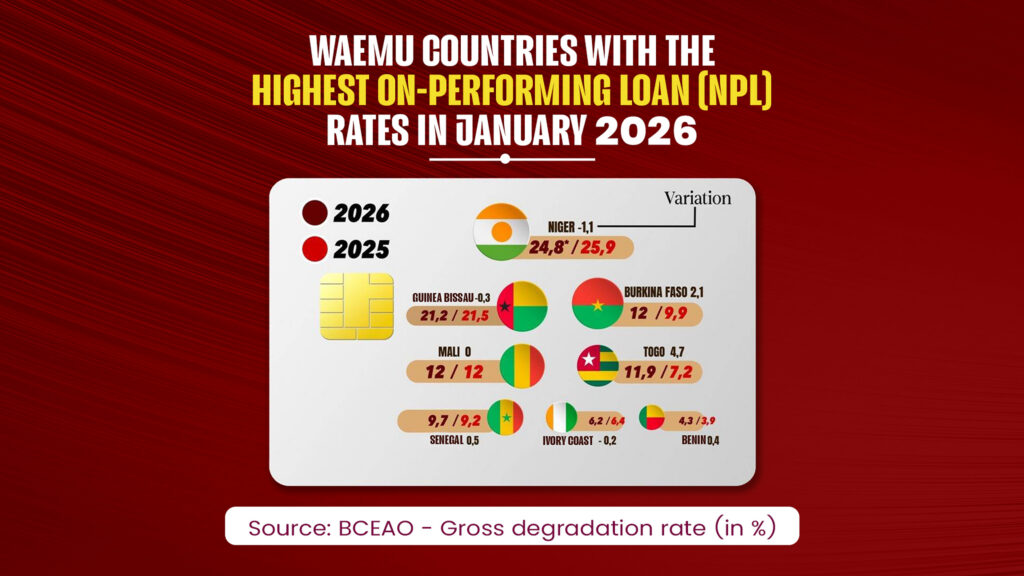

Despite marginal improvements in some areas, Niger remains the most vulnerable economy within UEMOA’s banking system. Its NPL ratio—a measure of loans in default—hit 24.8% in early 2026, the highest in the region by a significant margin.

This means nearly one in four loans disbursed in Niger is now non-performing, a figure that, while slightly improved from 25.9% in 2025, still underscores systemic fragility. The gap between Niger’s rate and the regional average highlights a severe structural vulnerability, exacerbated by persistent security threats and political instability.

A Tale of Two Subregions: Coastal Stability vs. Sahelian Struggles

The data reveals a sharp divide between UEMOA’s coastal economies and the Sahelian bloc, where Niger anchors a growing crisis.

The Sahel: A Zone of Escalating Risk

Beyond Niger, the Sahelian countries face mounting financial pressures:

- Mali & Burkina Faso: Both report NPL ratios of 12%, with Burkina Faso experiencing a sharp increase of 2.1 percentage points year-on-year.

- Guinea-Bissau: The country remains in critical territory with a 21.2% default rate.

The Coastal Bloc: Relative Resilience with Exceptions

By contrast, coastal nations maintain stronger loan portfolios, though not without concerns:

- Benin: Leads the bloc with the lowest NPL ratio at 4.3%.

- Côte d’Ivoire & Senegal: Report stable ratios of 6.2% and 9.7%, respectively.

- Togo: Bucking the trend with a sharp rise in defaults, jumping from 7.2% to 11.9% (+4.7 points).

Record Credit Growth Overshadowed by Rising Bad Debts

UEMOA’s total loan portfolio crossed a historic 40.031 trillion West African CFA francs in January 2026, marking a 4.7% annual increase. Yet this growth is clouded by deteriorating credit quality.

Non-performing loans surged to 3.631 trillion francs, pushing the coverage ratio—a measure of banks’ ability to absorb losses—down to 59%. This lag suggests that loan defaults are outpacing provisions, threatening financial stability.

Banks Retreat: Tighter Lending and Higher Barriers

In response to escalating risks, particularly in Niger and the Sahel, financial institutions are adopting defensive strategies:

- Stricter lending criteria: Higher down payments and collateral requirements are now common.

- Reduced risk appetite: Banks prioritize balance sheet safety over expanding credit to local SMEs, potentially stifling economic dynamism.

As UEMOA navigates this precarious moment, the Niger crisis and the spillover effects across the Sahel demand urgent attention. While the bloc’s overall financial system remains intact, the specter of liquidity crises looms large unless decisive measures are taken to restore confidence and stability.